Index

To purchase a second home from a private individual, you pay a registration tax of 9% on the cadastral value, in addition to €50 of cadastral tax and €50 of mortgage tax.

Calculating taxes for the purchase of a second home can turn into a real puzzle. Buying a second home involves a series of specific taxes and fees that vary from those for a primary residence. In fact, the law differentiates between properties intended for private use and those to be rented for long or short periods.

In addition to the IMU - the Single Municipal Tax - there are other expenses to keep in mind, from purchase costs to those for maintaining the property, with an average amount higher than that of primary residences.

As you may have guessed, we are faced with a tax scenario that is not at all simple to navigate. Taxes, we know well, can become a real bureaucratic nightmare that is difficult to keep track of. To help you avoid getting lost in this jungle of amounts, deadlines, and technicalities, we have decided to prepare a guide to taxes on your second home. You'll find all the information you need to know about the various fees you'll have to pay, from those due when you sign the contract to the annual recurring tax.

Second home purchase taxes for private individuals

Let's start with the purchase of a second home and the taxes for private individuals who will live there. There are three fees you need to pay when registering the deed of sale: registration tax, land registry tax, and mortgage tax. Let's look at them in detail:

- Registration tax, based on the so-called price-value system that we'll explain later, is equal to 9% of the property's cadastral value. Its final amount can never be less than €1,000;

- the land registry tax is €50;

- the mortgage tax, also €50

The registration tax is calculated considering the cadastral value of the property and can vary based on various factors, such as the type of home and the available tax breaks.

We remind you that for the purchase of the main residence, however, the registration tax amounts to 2% of the cadastral value of the property and is also calculated starting from a lower coefficient equivalent to 110, while the land registry tax and the mortgage tax are always €50. For the purchase of a second home, taxes are therefore significantly higher than for a first home due to the different calculation of the registration tax.

Second home purchase taxes for builders subject to VAT

If the second home is purchased from a builder or a construction company, the taxes to be calculated are different. In this case, in fact, VAT will also have to be considered, while the three taxes have a different value. Here's the summary:

- VAT equal to 10% of the value of the property, which reaches up to 22% for luxury properties (cadastral categories A1, A8 and A9);

- registration tax of €200;

- cadastral tax of €200;

- mortgage tax again of €200.

In the case of purchase by a company, therefore, there are three fixed costs and one variable, VAT, which depends on the purchase price of the property. In this table you will find a summary of the tax differences for purchasing from a private individual or a business:

For private individualsFor businesses subject to VATRegistration tax at 9% of the cadastral value (with price-value system)Registration tax of €200Cadastral tax of €50Cadastral tax of €200Mortgage tax of €50Mortgage tax of €200No VATVAT at 10% of the purchase price of the property

After having talked about the purchase of a second home and the related taxes, let's now analyze what are the annual taxes for owning the property.

Maintenance taxes for a second home

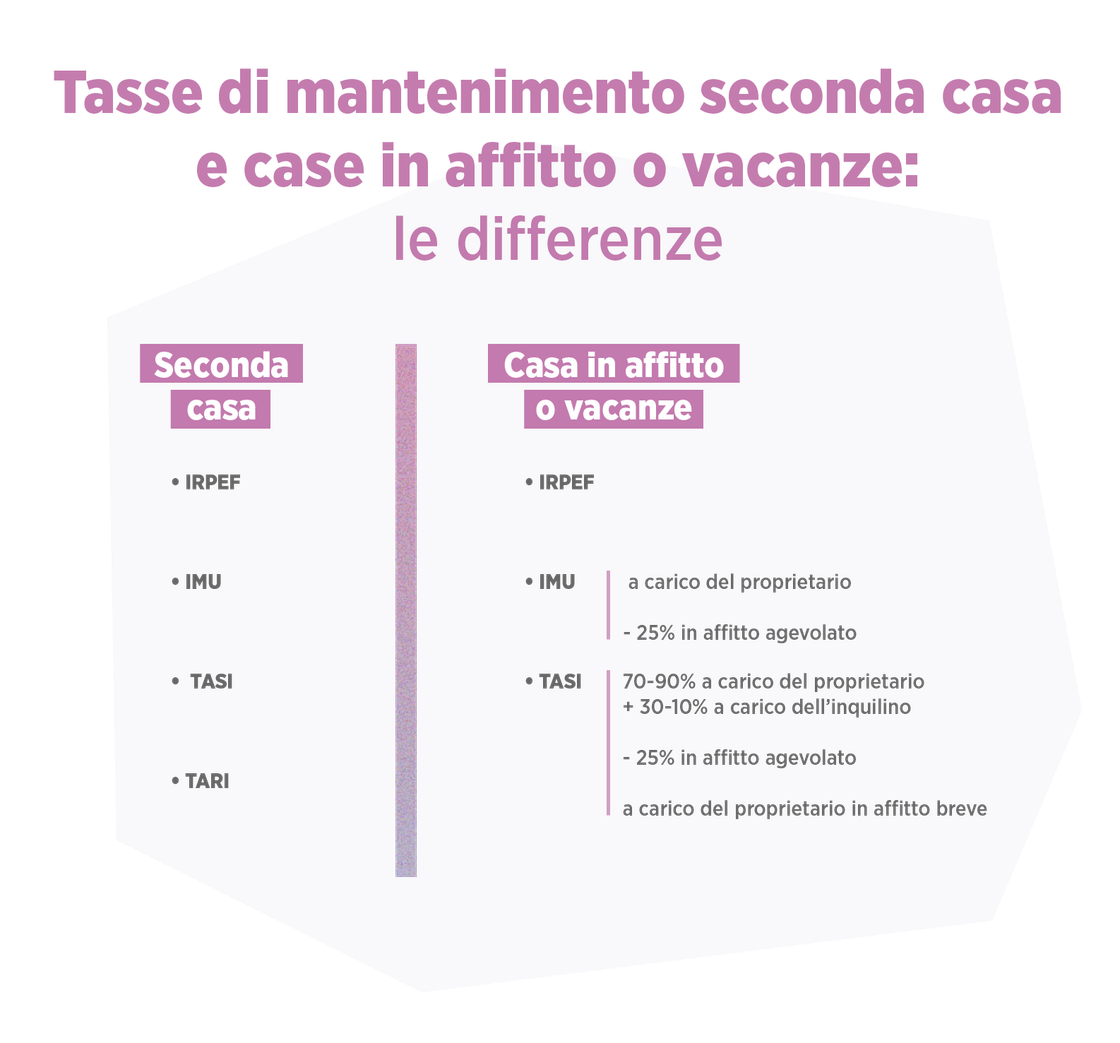

For the second home, the taxes to be paid during the year are four:

- IRPEF, in the case in which the second property is located in the same municipality as the main residence and is not rented, with the addition to the declared income of 50% of the cadastral income of the property revalued by 5% and increased by a third;

- the single municipal tax, the amount of which depends on various factors that you can find explained in this article of ours on how to calculate the IMU for the second home;

- the TASI, the Tax on Indivisible Services, i.e. the services made available by the municipality such as street lighting;

- the TARI, the waste tax, which weighs less and has a variable impact on the total.

If you decide to purchase a second property in the same municipality as your primary residence, you will also have to consider an increase in IRPEF in your annual expenses, at least as long as the building is not rented out.

To give a numerical example, let's imagine that the income from your property is equal to 1,000. With the revaluation it reaches 1,050 (with the addition of 5%) plus 350 (one third of the value), for a total of 1,400. You will have to add €700 to the annual IRPEF.

Maintenance taxes for rental homes and holiday homes

When the second property you own is intended for renting out, the tax situation changes again. The IMU remains the responsibility of the owner, but as for the TASI, the landlord pays between 70 and 90% of the total based on the tables established by the municipality where the building is located. The remainder is up to the tenant. However, if the tenant moves their residence to the property, the latter will not have to pay anything.

If we are talking about agreed rent, however, the tax framework changes again. Subsidized rent, regulated by Law 431 of 1998 on residential properties, was created to incentivize lower rental prices by providing tax discounts for owners. In this case, in fact, IMU and TASI are reduced by 25%.

As regards IRPEF, the greater of the cadastral income revalued by 5% and 95% of the monthly rent must be added to the annual tax calculation.

Finally, for short-term rentals of less than six months, therefore also in the case of rentals for tourist or holiday use, IMU and TASI are entirely borne by the owner.

Tax benefits for second homes

Now let's look at the tax benefits for second homes. Unfortunately, the law doesn't provide any special tax discounts for non-primary residences, but with a little care, you can manage to pay less.

For second home purchase taxes, it's important to specify during the purchase process that you're using the price-value system, which we mentioned earlier. This way, the final registration tax is calculated based on the cadastral value. Alternatively, the tax is set at 9% of the final purchase price (if you buy an apartment for €200,000, you'll pay €18,000) and is on average much higher. Furthermore, consider that the price-value allows you to save around 30% on notary fees. Please note: this system is only possible for sales between individuals, or in any case with sellers exempt from VAT.

As for maintenance taxes, you have already seen that with subsidized rent you save 25% on IMU and TASI.

If, however, you transfer the second home on loan for use to a first-degree relative(i.e. to your parents, or your children), the taxable amount on which you calculate the IMU and TASI is reduced by 50%. To take advantage of the reduction, you must regularly register the loan for use. It is therefore not enough for your child to de facto move into the property, but an official document will be necessary.

Example of calculation of the registration tax for private individuals

Let's go back for a moment to the taxes for the purchase of a second home for private individuals, in particular on the definition of the registration tax with the price-value system.

It is a somewhat complex calculation. complicated that takes into account the tables of cadastral income that we have already discussed in our blog. Taking the cadastral income of the property you are interested in, we must apply a 5% revaluation and multiply by the fixed coefficient of 120. On the figure we obtain, we then calculate the 9% registration tax.

As we said previously, the cadastral tax can never be less than €1,000. If, at the end of the calculations, the result is a lower value, it will be rounded up to this figure.

Let's take a numerical example and assume a property with a cadastral income of 1,000. The steps to follow are these:

we calculate the 5% revaluation and arrive at a value of 1,050;

we multiply by the fixed coefficient 120 and obtain 126,000;

the registration tax will be equal to 9% of 126,000, and therefore €11,340.

To this figure we must then add the land registry tax and the mortgage tax, bringing the total amount to €11,440.

Now let's imagine calculating the registration tax based on the purchase price. Let's go back to the figures we've already seen and imagine that you've reached an agreement with the private seller, not subject to VAT, to close the sale at €200,000. The tax therefore amounts to €18,000. Compared to the price-value calculation, you will therefore pay €4,600 more for the registration tax, plus other taxes.

Finding your way through the tax maze is never easy, but we hope this article has helped you define the taxes on your second home. Now that you know more, you're ready to look for your new home. Our real estate listings platform offers you numerous offers available immediately in Milan, Turin, Florence, Rome, Bologna, and Verona. Start looking for the best deal now!

Calculating taxes for buying a second home can be a real headache. Buying a second home involves a series of specific taxes and fees that vary from that of a primary residence. The law, in fact, differentiates between properties intended for private use and those to be rented for long or short periods.

In addition to the IMU - the Single Municipal Tax - there are other expenses to keep in mind, from purchase costs to those for the maintenance of the property, with an average amount higher than that of primary residences.

As you may have guessed, we are faced with a tax scenario that is not at all simple to navigate. Taxes, we know well, can become a real bureaucratic nightmare that is difficult to keep track of. To help you avoid getting lost in this jungle of amounts, deadlines, and technicalities, we have decided to prepare a guide to taxes on your second home. You will find all the information relating to the various charges to be paid, from those due at the time of signing the contract to the recurring annual taxation.

Second home purchase taxes for private individuals

Let's start from the phase of purchasing the second home and the taxes for private individuals who will live there. There are three fees to pay when registering the deed of sale: registration tax, land registry tax, and mortgage tax. Let's look at them in detail:

- Registration tax, based on the so-called price-value system that we'll explain later, is equal to 9% of the property's cadastral value. Its final amount can never be less than €1,000;

- the land registry tax is €50;

- the mortgage tax, also €50

The registration tax is calculated considering the cadastral value of the property and can vary based on various factors, such as the type of home and the available tax breaks.

We remind you that for the purchase of the main residence, however, the registration tax amounts to 2% of the cadastral value of the property and is also calculated starting from a lower coefficient equivalent to 110, while the land registry tax and the mortgage tax are always €50. For the purchase of a second home, taxes are therefore significantly higher than for a first home due to the different calculation of the registration tax.

Second home purchase taxes for builders subject to VAT

If the second home is purchased from a builder or a construction company, the taxes to be calculated are different. In this case, in fact, VAT will also have to be considered, while the three taxes have a different value. Here's the summary:

- VAT equal to 10% of the value of the property, which reaches up to 22% for luxury properties (cadastral categories A1, A8 and A9);

- registration tax of €200;

- cadastral tax of €200;

- mortgage tax again of €200.

In the case of purchase by a company, therefore, there are three fixed costs and one variable one, VAT, which depends on the purchase price of the property. In this table you will find a summary of the tax differences for purchasing from a private individual or a business:

For private individualsFor businesses subject to VATRegistration tax at 9% of the cadastral value (with price-value system)Registration tax of €200Cadastral tax of €50Cadastral tax of €200Mortgage tax of €50Mortgage tax of €200No VATVAT at 10% of the purchase price of the property

After having talked about the purchase of a second home and the related taxes, let's now analyze what are the annual taxes for owning the property.

Maintenance taxes for a second home

For the second home, the taxes to be paid during the year are four:

- IRPEF, in the case in which the second property is located in the same municipality as the main residence and is not rented, with the addition to the declared income of 50% of the cadastral income of the property revalued by 5% and increased by a third;

- the single municipal tax, the amount of which depends on various factors that you can find explained in this article of ours on how to calculate the IMU for the second home;

- the TASI, the Tax on Indivisible Services, i.e. the services made available by the municipality such as street lighting;

- the TARI, the waste tax, which weighs less and has a variable impact on the total.

If you decide to purchase a second property in the same municipality as your primary residence, you will also have to consider an increase in IRPEF in your annual expenses, at least as long as the building is not rented out.

To give a numerical example, let's imagine that the income from your property is equal to 1,000. With the revaluation it reaches 1,050 (with the addition of 5%) plus 350 (one third of the value), for a total of 1,400. You will have to add €700 to the annual IRPEF.

Maintenance taxes for rental homes and holiday homes

When the second property you own is intended for renting out, the tax situation changes again. The IMU remains the responsibility of the owner, but as for the TASI, the landlord pays between 70 and 90% of the total based on the tables established by the municipality where the building is located. The remainder is up to the tenant. However, if the tenant moves their residence to the property, the latter will not have to pay anything.

If we are talking about agreed rent, however, the tax framework changes again. Subsidized rent, regulated by Law 431 of 1998 on residential properties, was created to incentivize lower rental prices by providing tax discounts for owners. In this case, in fact, IMU and TASI are reduced by 25%.

As regards IRPEF, the greater of the cadastral income revalued by 5% and 95% of the monthly rent must be added to the annual tax calculation.

Finally, for short-term rentals of less than six months, therefore also in the case of rentals for tourist or holiday use, IMU and TASI are entirely borne by the owner.

Tax benefits for second homes

Now let's look at the tax benefits for second homes. Unfortunately, the law doesn't provide any special tax discounts for non-primary residences, but with a little care, you can manage to pay less.

For second home purchase taxes, it's important to specify during the purchase process that you're using the price-value system, which we mentioned earlier. This way, the final registration tax is calculated based on the cadastral value. Alternatively, the tax is set at 9% of the final purchase price (if you buy an apartment for €200,000, you'll pay €18,000) and is on average much higher. Furthermore, consider that the price-value allows you to save around 30% on notary fees. Please note: this system is only possible for sales between individuals, or in any case with sellers exempt from VAT.

As for maintenance taxes, you have already seen that with subsidized rent you save 25% on IMU and TASI.

If, however, you transfer the second home on loan for use to a first-degree relative (i.e. your parents, or your children), the taxable amount on which you calculate the IMU and TASI is reduced by 50%. To take advantage of the reduction, you must properly register the loan for use. It is therefore not enough for your child to de facto move into the property, but an official document will be necessary.

Example of calculation of the registration tax for private individuals

Let's go back for a moment to the taxes for the purchase of a second home for private individuals, in particular on the definition of the registration tax with the price-value system.

It is a somewhat complex calculation. complicated that takes into account the tables of cadastral income that we have already discussed in our blog. Taking the cadastral income of the property you are interested in, we must apply a 5% revaluation and multiply by the fixed coefficient of 120. On the figure we obtain, we then calculate the 9% registration tax.

As we said previously, the cadastral tax can never be less than €1,000. If, at the end of the calculations, the result is a lower value, it will be rounded up to this figure.

Let's take a numerical example and assume a property with a cadastral income of 1,000. The steps to follow are these:

we calculate the 5% revaluation and arrive at a value of 1,050;

we multiply by the fixed coefficient 120 and obtain 126,000;

the registration tax will be equal to 9% of 126,000, and therefore €11,340.

To this figure we must then add the land registry tax and the mortgage tax, bringing the total amount to €11,440.

Now let's imagine calculating the registration tax based on the purchase price. Let's go back to the figures we've already seen and imagine that you've reached an agreement with the private seller, not subject to VAT, to close the sale at €200,000. The tax therefore amounts to €18,000. Compared to the price-value calculation, you will therefore pay €4,600 more for the registration tax, plus other taxes.

Finding your way through the tax maze is never easy, but we hope this article has helped you define the taxes on your second home. Now that you know more, you're ready to look for your new home. Our real estate listings platform offers you numerous offers available immediately in Milan, Turin, Florence, Rome, Bologna, and Verona. Start looking for the best deal now!