Index

A joint home is a property shared by two or more people, each of whom owns a specific share of the property. Co-owning a house is a natural step for many couples who decide to move in together. It is a sign of mutual trust and a strong guarantee of unity and sharing.

If you are also about to purchase a property with another person, a brief summary of how co-ownership works, the advantages and disadvantages of buying half a house jointly, and the costs of the operation might be useful. To help you clarify the topic, we at Casavo answer the most common doubts in this complete guide on the subject.

The methods for co-owning a house

Before proceeding with the pros and cons, let's see what the steps are to achieve a jointly owned house. First of all, anyone can decide to purchase a property with another person, even without blood ties. The only requirement is that both parties are aware of the choice.

We can identify two fundamental methods of joint ownership:

- through purchase with direct participation of the two owners;

- with subsequent deed if one of the two people involved takes over after the purchase. In this case, a further deed will be necessary, which may be a sale or a donation.

Then there are cases in which co-ownership of the property derives from a previous deed, for example from a declaration in a preliminary contract or from a marriage in community of property. In this case, in fact, the spouses are always joint owners of 50% of what was acquired after the wedding, except in the cases indicated in article 179 of the civil code.

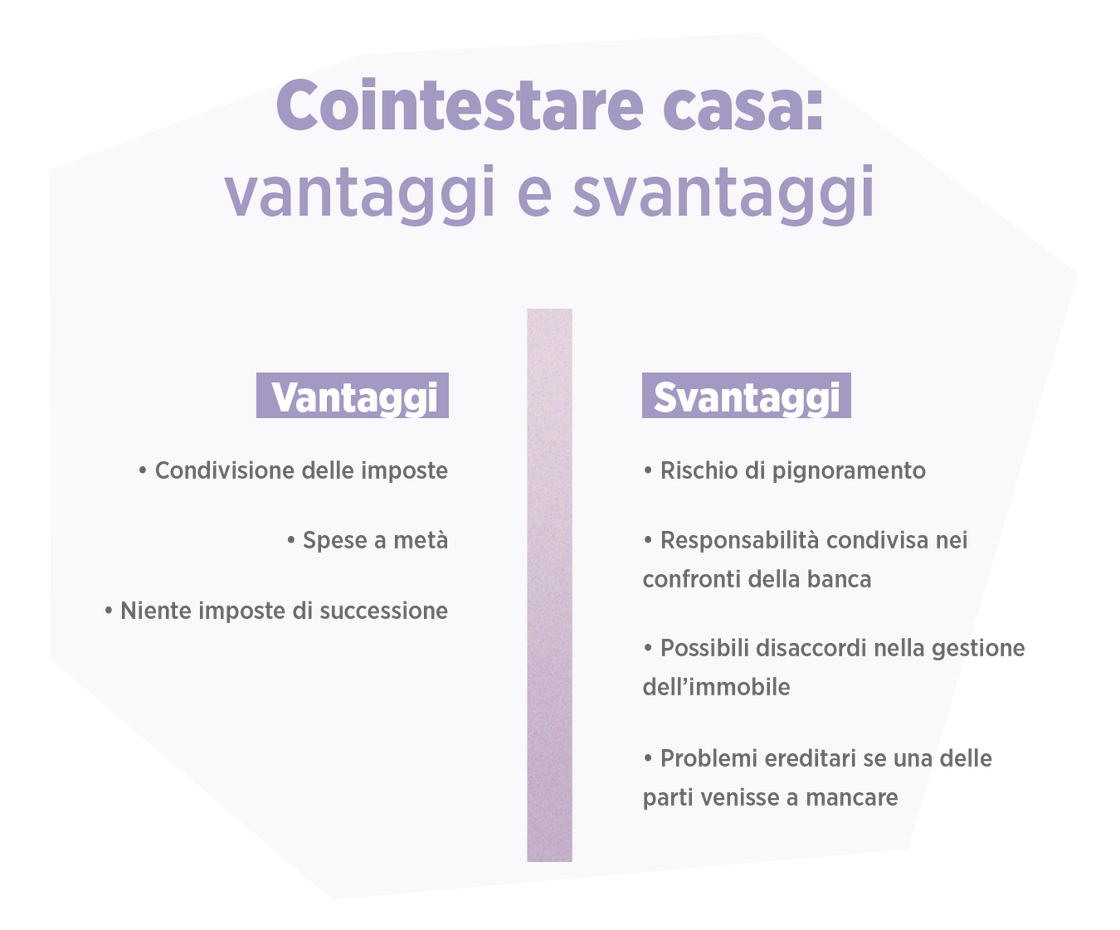

Jointly owned house: what are the advantages

Buying half a house jointly has indisputable advantages in terms of costs compared to a single purchase. A young couple today has many good reasons to buy a property together, starting with the first-home bonus for young people. Let's see what the pros of joint ownership are.

Division of expenses

The first advantage of a jointly owned home is the division of expenses. If it's a purchase with direct participation, you can split the budget to buy your first home with the other person involved. This doesn't just include the down payment and mortgage payments, but also all the taxes and notary fees, as well as any maintenance fees and costs associated with ownership.

Reduction of inheritance costs

If the house is jointly owned by people who share a family relationship, in the event of the death of one of the two people, there will be no inheritance costs. Therefore, no transfer of ownership between husband and wife, or between co-owner brothers and sisters.

Disadvantages of joint ownership

Deciding to buy half a house jointly is not all savings and new opportunities, however. There are in fact some disadvantages that we cannot help but talk about.

Risk of foreclosure

If one of the two co-owners finds himself having to respond in court for his debts, the judge could order the foreclosure and forced sale at auction of the shared home. The uninvolved party would therefore be deprived of the property and would receive their share back after the sale.

Liability towards the bank

In the case of a mortgage for the purchase, the two jointly owned parties are responsible towards the bank in the event of default.

Disagreement in the management of the property

Sharing ownership of a property also means being joint holders of all decisions to be made regarding its ordinary and extraordinary administration. And, obviously, the parties involved will not always agree. Whether it's a renovation project with or without tax breaks or a simple choice of furniture, the risk of a dispute is lurking. The situation becomes even more complicated when the heirs take over.

Inheritance problems

In the event that one of the two co-owners passes away, his share would pass to the heirs, who may obviously be more than one. The problems in this case arise above all from the difficulty in managing a house jointly owned by multiple parties, moreover different from the two who had initially expressed the desire for joint ownership.

A common example is that of the second home by the sea which is passed down from generation to generation until it is shared by a very large group of relatives of various degrees including siblings, cousins and nephews.

How much does it cost to co-own a house

Now that we have considered the pros and cons, all that remains is to analyze what the expenses of a jointly owned house are. We know that co-ownership of a property can arise from a purchase with direct or subsequent participation, or from a donation. The two cases have different costs, especially regarding the registration tax.

In the case of a donation, in fact, the basic tax is 8% of the value of the asset, but it varies if the people involved are related. Here's how:

- If the donation is between parents and children or between spouses, the amount drops to 4% and only on the value exceeding one million euros. Therefore, on a property worth one million and fifty thousand euros, a 4% tax would be paid only on €50,000;

- for brothers and sisters, however, the rate is set at 6% for the value exceeding €100,000;

- for other relatives up to the fourth degree a 6% tax is considered on the entire value of the property.

In the case of a sale in favor of a person who will become joint owner, however, the registration tax will be paid as for any other real estate sale. The rate will therefore be 2% of the cadastral value for the first home and 9% for the second.

Now that you have a clearer idea of how joint ownership works, you can immediately start looking for a new home to share with the person of your choice. If you haven't yet found the property that sparked your dream, take a look at Casavo's listings and start imagining your future now.